+91 8977930046

Your Money.

Managed, Guided, and Grown.

Savart helps you invest better, plan smarter, and grow faster with a unified ecosystem.

How much do you plan to invest

the next 12 months?

Our recommendation for you

Savart XLite

A smart start for new investors with expertly curated mutual funds, reviews, and ongoing portfolio care.

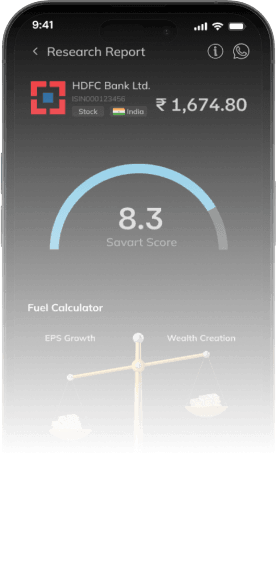

Know what to buy, when to sell

Power through the stock market with confidence.

4 Lakh+

Users

₹4500 Cr

Assets under advice

SEBI

Registered

19.5%

CAGR in 5 Years

Achieve Your Goals, Live Your Dream Life

Build the wealth you need today to live the life you envision tomorrow

3.9

4.0

I used to make losses investing on my own. After joining Savart, things turned around fast. Their advice is on point, and I’ve already recovered my subscription fee. It’s been a great decision.

Thiyagarajan

IT Professional

At first, I didn’t understand what Savart was about. But once I spoke to their team, everything made sense. The advice is simple and clear, and it’s helped me invest with more confidence.

Chandra Sekar

Businessman, Muscat

I found Savart when I was confused about where to invest. Their team is always helpful and patient, and their advice has really worked for me. I feel more confident with my money now.

Dr. Rashika Reddy

Doctor

Even during market ups and downs, Savart helped me get good returns with low risk. I’ve been happy with the results and would definitely recommend them to others.

Ravi Kumar

Geologist

Savart’s stock suggestions have worked really well for me. Their timing on when to enter and exit investments has saved me from losses. Totally worth it.

Poorna Chandra

Software Professional

I’ve been with Savart since 2019 and the experience has been great. They give me a portfolio that fits my needs and always reply quickly when I have questions.

Dr. Prashanth Appala

Doctor, Coal India Limited

I used to get confused with all the investment options out there. Savart made it easy with advice that matches my goals. The app is simple to use and their support is great too.

Kashish Suneja

Software Engineer